🎖️ Philip Salter, Founder

The King’s Birthday Honours landed last week, which gives me an excuse to return to ask the same question we’ve been asking since 2021: how many of these honours go to the people inventing and building things?

Five years ago, in our report Honours for Innovators, Ned Donovan and Anton Howes ran the numbers and found the answer was not many. We have now repeated the exercise across the last eight lists — every New Year and Birthday Honours since the end of 2022, more than 9,000 appointments to the Order of the British Empire — to see whether anything has shifted.

It hasn’t. Just one in ten citations mentions anything to do with innovation, science or industry, almost exactly where we found it in 2021. Strip out the broadest catch-alls of “industry” and “business” and it is lower still. Narrow it to the word “entrepreneurship” and it all but vanishes: 0.68% of honours. And these are generous counts — plenty of the citations we include are really for management or charitable work within a sector, rather than for invention in its own right.

As we argued in Honours for Innovators: “Given the current system, one would be forgiven for assuming that the surest way to an honour is to become a civil servant, politician, or philanthropist, or to achieve the fame that comes naturally to especially successful sports people, musicians, authors and actors.”

There are always honourable exceptions. In the latest list, our Patron Chris Hulatt, co-founder of Octopus, was made a CBE for services to entrepreneurship. More of this, please. Or, if the Government is feeling more ambitious, they might institute our dedicated order — what we called the Elizabethan Order — of genuinely equal standing to the OBE, with the same familiar four classes and a Sir or Dame at the top, awarded purely for invention and enterprise. It would cost around £66,000 a year: less than a single MP’s salary, for a payoff in status and aspiration many times larger.

This isn’t as radical as it might sound. Britain built its early reputation as the best place in the world to innovate partly by heaping status on inventors: the Society of Arts (now the RSA) struck medals to encourage them, monarchs granted them personal pensions, and there was even a chivalric order — the Royal Guelphic — that honoured the likes of Charles Babbage and William Herschel, the astronomer who discovered Uranus. It lapsed in 1837, not because the idea failed but because Queen Victoria could not inherit the crown of Hanover.

It’s time for a new chivalric order. This is the signal we need to give that Britain is serious about being the best place in the world to be a scientist, an inventor or a founder.

🔀 Mann Virdee, Head of Science and Technology

On Monday, the Government Office for Science published their updated five AI scenarios for 2030. It’s the first update to a set of scenarios originally developed in 2023 and first published last year — with the aim of helping policymakers plan for the future of AI.

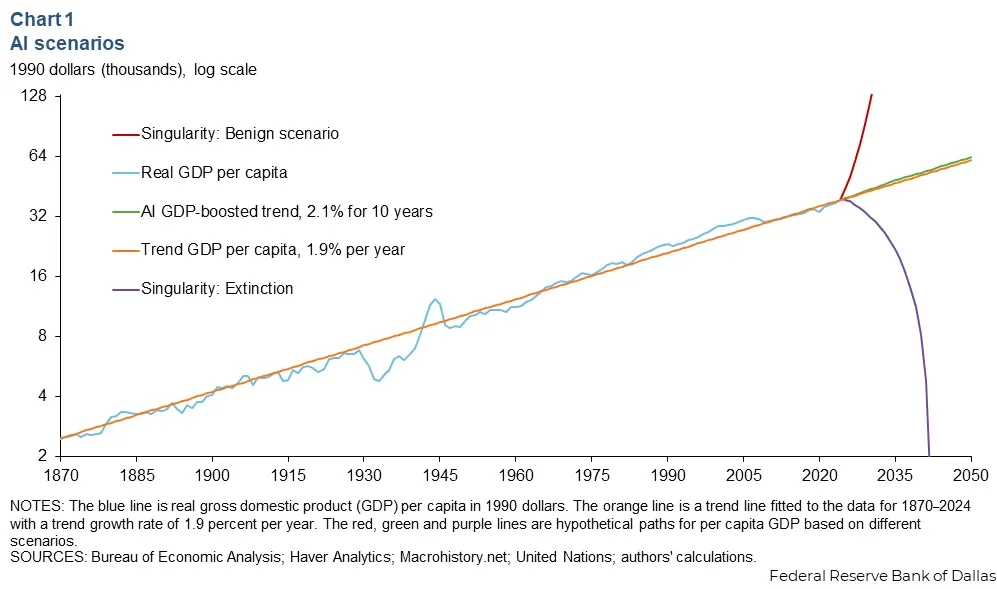

Before getting into the details of the five scenarios, there’s an important methodological point. People often believe that scenarios are attempts to predict the future — but that’s not true. Scenarios are a rigorous and methodical way to consider several imagined future situations which could come to pass, but they don’t have to happen in order to be useful. They’re designed to be different from one another, and their value lies in helping policymakers identify trends and useful courses of action across a wide range of potential outcomes. That’s to say, we should avoid the temptation to focus on the scenario we think is most likely because that’s not the purpose of such exercises. At the same time, they should still reflect plausible outcomes, otherwise you end up with AI scenarios like this unhelpful graph from the Federal Reserve Bank of Dallas.

How not to do AI scenarios (Source: Federal Reserve Bank of Dallas)

The scenarios outlined in the GO-Science report range from a ‘slow burn’, to ‘augmented growth’, to ‘take off’ — and provide a more nuanced picture than the graph above. The report looks at six ‘critical uncertainties’ for each scenario: capability, model access, security, adoption, labour displacement and global cooperation.

Across most scenarios, AI drives significant productivity gains, helps to transform public services and make them more accessible, and accelerates scientific breakthroughs in fields such as health and energy — which will likely become key drivers of Britain’s productivity growth.

At the same time, across all scenarios, even in the slowest, the nature of cognitive work changes significantly, with routine, execution-oriented tasks being automated. There’s also a risk that workers become overly reliant on AI and have trouble operating if it fails. Another finding that holds true across all scenarios is the uneven adoption of AI and the compounding effect that will have, with a bifurcation where some realise the tremendous potential of AI while others are left behind.

It may not be the most groundbreaking report, but should serve as a good tool to help policymakers think more systematically about the future of AI and its adoption.

⚡Ian Ng, Researcher

The Trump administration placed Anthropic’s Fable 5 under export control last Friday, barring foreign nationals from accessing it. Anthropic responded by disabling the model for all customers. The ban came a day after the Europe 2031 essay imagined precisely a world in which Washington rations AI exports as a geopolitical lever. AI Minister Kanishka Narayan drew the obvious lesson: “access to AI capabilities is crucial.”

Europe’s dilemma is rooted in having no frontier model of its own. Adopt American models and you cede control of the access lever; adopt them slower than the US and the productivity gap only widens. If the past year has demonstrated anything, it’s the value of sovereignty and autonomy.

We live in an economy defined by chokepoints. Just as the Netherlands has ASML and Taiwan TSMC, Britain must think about the leverage we can build. We do have a seat at the table as a signatory of Pax Silica and the AI Security Institute being one of the few trusted to evaluate Mythos. However, it does not guarantee access to frontier AI models. The US has already floated a “trusted partner” scheme granting close allies privileged access. The tiers are being drawn now, and Britain cannot be sure if it will retain such access in future.

Leverage cannot be built overnight. The nature of a chokepoint is that once built, it cannot be easily replicated. ASML took four decades and an extraordinary accumulation of tacit knowledge across 5,000 suppliers. But that is precisely the argument for doubling down now. Britain, through our higher education sector, still holds an edge on talent. Our universities produced the researchers behind DeepMind and Arm. Without strategic chokepoints of our own, it matters all the more that we sharpen the edge that we still have and do everything to retain that talent.

Keeping talent is not solely about money because Britain will not win a bidding war with American labs. It is about whether there is anything here to work on. For frontier researchers that means compute, and the gap is stark: Isambard-AI, our most powerful machine, ranks eleventh in the world, while the top three are all American exascale systems.

We are not going to out-spend Washington. Government funding for British compute — £1 billion for AIRR, £750 million for Edinburgh — is barely a tenth of the £22 billion Microsoft alone is putting into the UK. Accepting American capital is unavoidable, and any honest plan builds most of its capacity that way. But some must sit on a sovereign core — publicly held compute backing British firms directly. AIRR is how Britain avoids having to 'rent its AI future from abroad’.

If the shelving of the Edinburgh supercomputer and the pausing of OpenAI’s Stargate UK were not wake-up calls enough, the export ban on Fable 5 should be. Certainty over the long term funding is crucial to attracting investment and retaining talent. That requires fiscal discipline from the government — both resisting borrowing for day-to-day spending as well as resisting the urge to axe capital projects when money is needed elsewhere.

None of this delivers leverage Britain can wield alone. But the fundamentals built at home are what give us something to bring to a table we cannot dominate.