By Hugo Okada and Osian Guthrie

Endorsements

“The City of London clears 38% of global foreign exchange every single day, yet GBP-denominated stablecoins represent a fraction of a percentage of the global stablecoin market. This report gets to the heart of that gap. The holding caps, the unremunerated reserve requirements, and the broader regulatory caution risk smothering business use cases before they even exist. The UK has the talent, the infrastructure, and the track record — what it needs now is a stablecoin regime that matches that ambition.”

Sam Hinton-Smith — Head of International Public Policy & London Site Lead, Stripe

“The UK has a real opportunity to lead in stablecoins, but only if regulation is proportionate and competitive. This report captures what industry is seeing on the ground, namely that the right framework can unlock significant growth for British businesses, from cross-border payments to digital financial markets. It’s exactly the kind of informed, forward-looking contribution we need as British regulators and the Government shape the rules.”

Adam Jackson — Chief Strategy Officer, Innovate Finance, and Head of Digital Pound Foundation

“As legal advisers to firms navigating the UK’s incoming regulatory frameworks, we understand that the authorisation process takes planning, internal alignment and experienced input. The legal and technical infrastructure will be significant, and the implementation timeline is not to be underestimated. Businesses need a framework that is clear, workable and delivered in time. A regulatory regime that recognises this and supports innovation, ensuring that regulatory expectations scale appropriately as firms grow, while safeguarding stability, is critical. This report, grounded in practical experience and with practitioner-led contributions, provides informed views for the regulators. We are at a pivotal moment for the UK to take second-leader advantage, or for it to dissipate.”

Laura Clatworthy — Head of Digital Assets and Emerging Tech, Edwin Coe LLP

“The UK’s approach to stablecoin regulation is a defining test of its commitment to digital innovation that empowers ordinary people. British citizens are at the forefront of digital asset adoption globally, and they want to see the UK fulfil the Chancellor’s ambition of becoming a world-leading digital asset hub. That means delivering policies that actively enable progress rather than restrain it.”

Adriana Ennab — Director, Stand With Crypto UK

“It is genuinely encouraging to see such a deep and thoughtful piece of work on stablecoins. At the UK Cryptoasset Business Council, we are in no doubt that stablecoins will play a foundational role in the future of finance. This report shows just how clearly younger generations grasp this shift. They understand where finance is heading because they are growing up in a digital-first world.”

Simon Jennings — Executive Director, UK Cryptoasset Business Council

“The gap between how stablecoins actually work and how UK regulators propose to treat them remains too wide. Stablecoins are a new product, with a new legal structure, distribution model, and user relationship. This report makes that case with clarity and precision, drawing on the practical experience of firms building within the regime. It can help policymakers seize the huge opportunity in front of us.”

Tom Rhodes — Chief Legal Officer, Agant Finance

“Xapo Bank has had stablecoin rails integrated directly into bank accounts for three years. The question was never whether it could work — it was whether regulators would create the conditions for others to follow and whether the industry could meet those requirements. This report gives them a clear basis to do so, and the UK should take it seriously.”

Joey Garcia — Executive Director, Chief Strategy, Policy, Regulatory Affairs Officer, Xapo Bank

Foreword: Lord Holmes of Richmond OBE

We are living in uncertain geopolitical and macroeconomic times. Faced with this, the ‘safe’ response could well be to retreat to traditional financial services approaches. Yet, as this report highlights, we must instead look to new technologies to enable potentially transformational solutions.

Stablecoins are a prime example. They are no longer a niche asset class. Instead, they represent the future of payments, settlement and efficient movement of value in modern financial markets. However, the United Kingdom stands at a crossroads. While adoption is well underway globally, uncertainty around regulation here continues to delay progress.

As I recently raised in the House of Lords, there is a clear and present danger that we fail to distinguish between volatile, unbacked cryptoassets — which are essentially investments — and fiat-backed stablecoins, which are digital money. Regulating digital money as though it were a speculative asset risks making it impractical to use. If firms face extra regulatory hurdles simply for using stablecoins instead of cash, they will not use them, and the UK’s wider digital asset ambitions will struggle to get off the ground.

The data in this report reinforces a point we hear repeatedly across the ecosystem, that the biggest barrier to adoption isn’t the technology, it’s regulatory clarity.

We have seen how US dollar-denominated stablecoins are, in effect, exporting US Government debt. A well-designed sterling-denominated stablecoin could do the same for the UK. However, if we do not get this regulation right, dollarisation becomes more than just the default, and we risk becoming a ‘fly-over’ jurisdiction for digital assets.

I welcome the recent ramp-up in engagement from the Financial Conduct Authority and the Bank of England, but at the same time, we must ensure that we avoid both double regulatory burdens and regulatory gaps. This paper sets out a compelling case for a principles-based, outcomes-focused regulatory regime. It argues that safety and security must remain paramount, but that growth requires proportionate risk tolerance. We do not want to design a regulatory regime that renders the UK irrelevant.

The UK has a history of leadership in fintech. We are celebrated for our sandbox approach to regulation — and sandboxes are indeed effective. But looking at the scale of the opportunity presented by stablecoins, let us not rest on our laurels but rather fully grasp this technology.

By making a positive, evidence-based case for a pro-innovation regime, this report gives policymakers and regulators exactly what they need: a clear, actionable path forward. The future of money in the UK will be shaped by decisions made now — and this report should inform them.

Lord Holmes of Richmond OBE — Member of the All-Party Parliamentary Group on FinTech and the All-Party Parliamentary Group on Digital Identities

Executive Summary

Stablecoins are a growing asset class within the financial services industry, and their diffusion throughout the economy could bring significant benefits for consumers and businesses alike.

Despite their infancy, different countries are already moving quickly to establish regimes to regulate stablecoins. Broadly speaking, these regimes try to balance innovation and flexibility against consumer protections and financial system integrity. In the United Kingdom, the specific rules that will eventually regulate stablecoins are still being finalised. We believe that while a good start has been made — one which signals that the UK is receptive to the growth of stablecoins as an asset class — there remains room for significant improvements on both the protection and innovation sides.

This briefing paper aims to highlight the issues with the current proposed regime from the perspective of entrepreneurs in the UK, while offering constructive solutions to regulators. We make the following recommendations for how the UK can create a competitive regulatory regime for stablecoins — in which consumers are protected, issuers have freedom to innovate, and businesses reap their benefits.

Adopt a principles-based approach to regulating stablecoins. Firms in emerging sectors need flexibility to adapt technology and business models. As such, regulators should adopt higher-level, principles-based rules that support innovation while still securing core regulatory outcomes. This can likely be achieved through alignment in approaches between the Financial Conduct Authority (FCA) and the Bank of England (BoE).

Scrap universal redemption. Universal on-demand redemption misunderstands how stablecoin issuers operate and should be replaced with a model reflecting the current structure of issuers, distribution partners, and users.

Remove bank-like capital rules. Capital requirements designed for banks are inappropriate for fully backed issuers, and should be replaced with oversight focused on reserve quality and transparency.

Allow flexible redemptions. Flexible redemption timelines should be introduced, as seen in the GENIUS Act, to support issuer sustainability and market resilience.

Lift holding caps. The £20,000 (individual) and £10 million (corporate) limits should be lifted, as they are currently overly restrictive and risk stifling institutional and business-to-business innovation, as well as creating secondary market price volatility and liquidity shocks.

Explain reserve split. The reasoning behind the 60:40 reserve rule should be clarified, and regulators should consider remunerating a portion of the 40% held at the BoE to maintain commercial viability.

Exempt small businesses. As happens with payment services and other regulatory regimes, small businesses operating within the stablecoin market should be exempt from more stringent regulatory expectations to allow them to balance costs and innovation, which is particularly important in a nascent and fast-developing industry.

introduction

Finance is entering a new era, with stablecoins rapidly emerging as a core component of modern payments and settlement systems. According to Citi, the total market capitalisation of stablecoins could reach up to $4 trillion by 2030. The United States is capitalising on their benefits, with US dollar-denominated stablecoins currently representing around 99% of the market. Despite its position as the world’s largest foreign exchange hub — clearing 38% of all daily foreign exchange transactions in 2025, equivalent to around £3.5 trillion per day — the United Kingdom has only just legislated its framework, the Financial Services and Markets Act 2000 (Cryptoassets) Regulations 2026. However, the operational rules of both the FCA and BoE regimes are subject to change. Developing functional regulation is therefore a matter of national importance to ensure the UK remains competitive in a rapidly growing market.

The paper examines how such a regime could position the UK at the forefront of financial innovation, highlighting opportunities for entrepreneurs, the risks of inaction, and perspectives from industry leaders driving this change. We begin with an overview of what stablecoins are and the advantages they can offer, before sketching out the current stablecoin landscape and detailing how different regulatory regimes are being applied to stablecoins around the world. Finally, we conclude with a series of policy recommendations that would allow the UK to play a competitive role in the global stablecoin market.

What are stablecoins?

Stablecoins are digital representations of existing assets. Broadly speaking, there are two types of stablecoins: collateralised stablecoins, which are backed by real-world assets (RWAs) such as government treasuries and cash, or by more volatile instruments such as gold or Bitcoin; and algorithmic stablecoins, which maintain their peg synthetically through advanced mechanisms, including delta-neutral trading strategies.

This paper will focus on the former, specifically fiat stablecoins backed 1:1 by government treasuries and other high-quality liquid assets (HQLAs). These stablecoins are ‘pegged’ 1:1 to a currency, meaning the issuer will issue or redeem them at a rate of one stablecoin for one unit of currency. A single sterling-denominated stablecoin is worth exactly £1, while a dollar-denominated one is worth $1, and so on.

what advantages do stablecoins have?

Stablecoins offer a range of benefits to consumers and businesses alike, including:

Near-instant, around-the-clock settlement. Stablecoins allow people to send payments of any size, anytime, near-instantly, without bouncebacks and internal delays.

Financial inclusivity. Stablecoins grant people living in unstable economies and unbanked areas access to trustworthy currencies with just a smartphone and internet connection.

Programmability. Stablecoins can execute rules and automate transactions directly through smart contracts, enabling seamless, condition-based financial activity.

Cost-effectiveness. Stablecoin fees are extremely low, typically less than $0.10 per transaction globally, while traditional banks can charge up to a £30 flat fee, or 2–4% on international transactions.

Unlike traditional cross-border financial networks such as SWIFT and domestic settlement systems such as CHAPS — which are limited by banking hours, intermediaries, and multi-day settlement processes — stablecoins enable funds to move globally within seconds and at extremely low costs. Most stablecoin transactions can be made for less than $0.10 per transaction, irrespective of transaction size. Conventional international payments are far more costly, with high-street banks typically charging up to £30 per transaction or a percentage markup of 2–4% — substantial costs when transferring larger sums. In addition, such payments risk bouncebacks and other delays. In fact, nearly half of all cross-border payments administered through SWIFT take over an hour to complete, with 8% taking more than one business day. Stablecoins, therefore, offer meaningful cost and efficiency improvements, particularly for business-to-business (B2B) transactions. For startups in particular, which generally place a premium on low overheads and swift access to capital, this reduces working-capital strain and lowers friction in import and export payments, which can translate into higher productivity and competitiveness.

Stablecoins also offer superior financial inclusivity compared to traditional banking systems. With only a smartphone and an internet connection, individuals can access digital equivalents of major, trusted currencies such as the US dollar, Japanese yen, or euros directly on the blockchain. This removes many of the barriers associated with traditional banking, including lengthy and restrictive know-your-customer (KYC) and anti-money-laundering (AML) processes — providing a vital financial lifeline to the 1.4 billion unbanked individuals worldwide, as well as those living in politically unstable or hyperinflationary economies. For the UK’s economy, this would heighten demand for sterling-denominated stablecoins, strengthening sterling’s relevance in global digital payments.

Crucially, this inclusivity does not come at the expense of transparency. Stablecoins record all transactions immutably on the blockchain in real time, providing an open and verifiable record of transfers — significantly enhancing accountability. This is particularly relevant because a considerable proportion of illicit activity on the blockchain has been denominated in stablecoins — a by-product of the increased accessibility and use of such cryptoassets — highlighting the need for a comprehensive regulatory regime which monitors such activities, and prosecutes accordingly.

Another compelling advantage of stablecoins is their programmability. Indeed, this facet introduces a new dimension to money — enabling automated, conditional, and self-executing payments through smart contracts. This would allow for seamless, rule-based financial activities that are currently unachievable with conventional financial assets. Examples might include automatically releasing funds upon goods delivery in a supply chain, instantly distributing royalties to multiple creators, or triggering real-time insurance payouts based on verified data like weather events.

While the benefit of programmability may seem niche, it highlights the potential for entrepreneurs to unlock novel applications of money that are difficult to imagine today. Just as the most impactful internet applications of today might have seemed unimaginable in 2000 — such as a platform for sleeping at other people’s houses or instant online food delivery — the most useful applications of stablecoins may not yet be obvious.

As will be outlined later, institutions are already benefiting from stablecoins. The question for the UK, therefore, is whether we will create the conditions for entrepreneurs to build in this market — capturing the jobs, innovation, and economic activity that comes with it — or whether we will continue to watch consumers and businesses in other economies be the primary beneficiaries of stablecoins.

What does the current stablecoin landscape look like?

While still niche in relative terms, the adoption of stablecoins is well underway and shows no signs of slowing down. Major American payment networks — including Visa and Mastercard — are integrating stablecoins into their infrastructure. In fact, according to Jeremy Allaire, the CEO of Circle, a major stablecoin issuer, USDC’s transaction volume reached $8.4 trillion in January 2026 alone, nearly half of Visa’s yearly volume. Leading merchants such as Walmart and Amazon are also exploring their use, with the potential to save billions of dollars annually in transaction fees. Meanwhile, in February 2026, Fidelity Investments launched its own institutional-grade stablecoin. Similarly, a consortium of major international banks — including Goldman Sachs, Bank of America, Deutsche Bank, and UBS — is reportedly examining the creation of stablecoins pegged to G7 currencies. According to a report from EY, 13% of financial institutions and corporations worldwide already use stablecoins, with a further 54% planning to adopt them within the next 6–12 months. Reflecting this momentum, the total market capitalisation of stablecoins now stands at around $300 billion, with Citi projecting a base-case scenario of $1.9 trillion and a bull-case scenario of $4 trillion by 2030.

Growing institutional adoption of stablecoins continues to reinforce their utility and thus further bolsters underlying market demand. But stablecoins are not only being looked at by institutions. Due to the stablecoin backing process, in which stablecoin issuers hold the majority of the principal in (usually short-term) government bonds, governments increasingly view stablecoins as an alternative and latent source of demand for government debt. In fact, by facilitating demand for stablecoins — such as through favourable regulatory regimes — governments can unlock additional demand for their debt. For example, Tether, which issues USDT, the world’s largest stablecoin by market cap, already outranks the likes of Germany and Israel in terms of US Treasury holdings.

The promise of stablecoins in this respect has not gone unnoticed. In August 2025, US Treasury Secretary Scott Bessent noted the potential for stablecoins to become an important source of demand for US Government bonds. Last year alone, around $9.2 trillion of US debt matured, and the US Government is now spending more on interest payments than on national defence (nearly $1 trillion annually). If stablecoin issuance reaches upwards of $1 trillion in the next five years — Bessent himself has cited projections of up to $3.7 trillion — the additional demand could push up bond prices, and in turn lower yields, allowing the US government to roll over debt more cheaply.

With all this in mind, it is not surprising that several jurisdictions have already implemented regulatory regimes for stablecoins — including the US, the European Union, Japan, Hong Kong, and Singapore. Of these, the GENIUS Act in the US is the most ‘pro-innovation’ — facilitating entrepreneurship and innovation to a higher degree, with obvious tradeoffs in terms of financial stability that will be touched on later. It is clear that stablecoins are being adopted regardless by corporations, governments, individuals and entrepreneurs alike on technological grounds. It is therefore in the UK’s interest to embrace the innovative capacity of stablecoins, without falling into the trap of blindly following America’s approach.

Box 1. How Central Bank Digital Currencies differ from stablecoins

Central Bank Digital Currencies (CBDCs) are a similar concept to stablecoins. CBDCs are digital versions of a nation’s fiat currency, but are issued and managed by the central bank, rather than private companies, and are intended to provide a secure and reliable form of public money. While this may sound appealing at first, we argue that CBDCs are inferior to stablecoins, and, in any case, that CBDCs and stablecoins need not be mutually exclusive.

One of the primary drawbacks of CBDCs is that they are inherently closed-loop systems — created by a central bank, and therefore almost inherently less disposed to innovation. As expert Joey Garcia informed us during the course of this research, prioritising CBDCs over stablecoins is analogous to attempting to build a closed-loop intranet when the internet was already gathering momentum in the early 2000s. Had the UK done so, it likely never would have produced companies such as Deliveroo, ASOS and Revolut. Just as with the internet, much of the value in stablecoins comes from the open-loop, global accessibility that they enable. CBDCs are intentionally confined to domestic monetary systems to preserve national control over money supply and capital flows, making cross-border interoperability difficult in an increasingly globalised and instant-payments landscape.

While CBDCs appear safer at first glance — backed by central banks and functioning like digital cash without requiring bailouts like stablecoins might — appropriate regulation could make stablecoins sufficiently secure while still enabling innovation. Both the regulatory frameworks and underlying risks will be explored later.

In this way, a setup in which CBDCs and stablecoins exist concomitantly may yield the best results. CBDCs may act as a wholesale layer for commercial banks and financial institutions to settle huge payments instantly and without risk, while private companies may issue stablecoins for use in apps, smart contracts and cross-border transactions. As a report from Imperial College London notes, CBDCs and stablecoins sit in different positions within the hierarchy of money, suggesting the possibility of harmonious existence between the two.

How are stablecoins being regulated around the world?

Being a relatively novel development with potentially profound economic consequences, regulators around the world have naturally paid close attention to the rise of stablecoins. It is essential that the risks of stablecoins to consumers and to wider financial stability are adequately understood. Crafting a regulatory regime that is too liberal concerning risk management protections could endanger financial stability if, for example, stablecoins are allowed to operate without stringent requirements for high-quality liquid reserves. A ‘run’ on such a stablecoin could force a firesale of its assets and cause contagion elsewhere in the financial system, as well as harming consumers holding said stablecoin. Moreover, widespread use of stablecoins could lead to unmanaged bank disintermediation, in which there is a flight from commercial bank deposits. Considering that fractional reserve banking (allowing banks to provide loans using deposits) underpins much of the UK’s economic activity, losing this credit-provisioning could seriously harm financial stability. However, as the Bank of England Governor noted recently, “it is possible, at least partially, to separate money from credit provision, with banks and stablecoins coexisting and non-banks carrying out more of the credit provision role.” He is also right to point out that it is important to consider the implications of such a change to create a productive regulatory environment.

In this respect, the UK’s ‘second-mover advantage’ can be seen as beneficial. As time goes on, we learn more and more about how this technology will impact the status quo. However, what was once a second-mover advantage has turned into more of a sixth- or seventh-mover advantage. While the quality of the regime certainly matters more than the speed at which it is instituted, further delays may serve to disadvantage the UK significantly.

First, given that jurisdictions such as the EU and the US are moving forward with clear frameworks, the UK risks losing investment, talent and influence. Entrepreneurs will gravitate to markets that offer the clearest regulatory certainty — potentially leaving the UK’s ambition to be a global cryptoasset hub unrealised. Startups seeking to innovate in line with non-existent regulations require regulatory guidance to know whether their business models are sustainable once a regime is implemented.

Moreover, the trend of digital dollarisation will only accelerate. Without a domestic alternative, British businesses and consumers will become increasingly reliant on offshore, dollar-linked systems — ceding control of future financial architecture to foreign entities outside the bounds of Britain’s regulatory orbit.

Finally, increased delay harms consumers. British citizens are already using unregulated stablecoin products. Continued delay leaves them exposed to significant risks without the proper safeguards and legal recourse that a domestic regime would provide.

For all of these reasons, the UK must ensure that its forthcoming implementation is as high-quality as possible. It has long been a global hub for financial services and innovation, with 38% of global foreign exchange flowing through London. The UK is home to 11% of the global fintech industry, having produced behemoths such as Revolut, Monzo, Starling and Wise in the last fifteen or so years alone. Sterling is currently the world’s fourth most traded currency, which is a testament to its international significance. However, we must not rest on our laurels. Sterling currently represents a fraction of a percentage of the stablecoin market cap — ground on which the UK needs to be competing in. There is a high risk of the UK fading more and more into economic irrelevancy, and ceding digital dominance to the US dollar on a massive scale, even more so than has already occurred.

But what does a productive regime for stablecoins actually look like in practice? In order to answer this, it is useful to survey the existing stablecoin regimes instituted by other jurisdictions.

The European Union’s MiCA Regulation

The EU was one of the first jurisdictions to roll out formal stablecoin regulations, covering various aspects of digital assets, including tokens, exchanges, and, crucially, stablecoins, to retain monetary sovereignty and financial stability for all 27 EU nations. The Market in Crypto-Assets (MiCA) Regulation aims to do this by enhancing transparency, mandating detailed whitepapers, independent audits, and reserve disclosures, while also banning undercollateralised and algorithmic stablecoins. MiCA has, in some ways, been positive for the stablecoin market — highlighting the EU’s support of stablecoins in principle, and laying the foundations for future frameworks. On the other hand, however, critics allege MiCA has discouraged growth within the EU stablecoin market, making it an unfavourable environment for both startups and established issuers.

Universal on-demand redemption

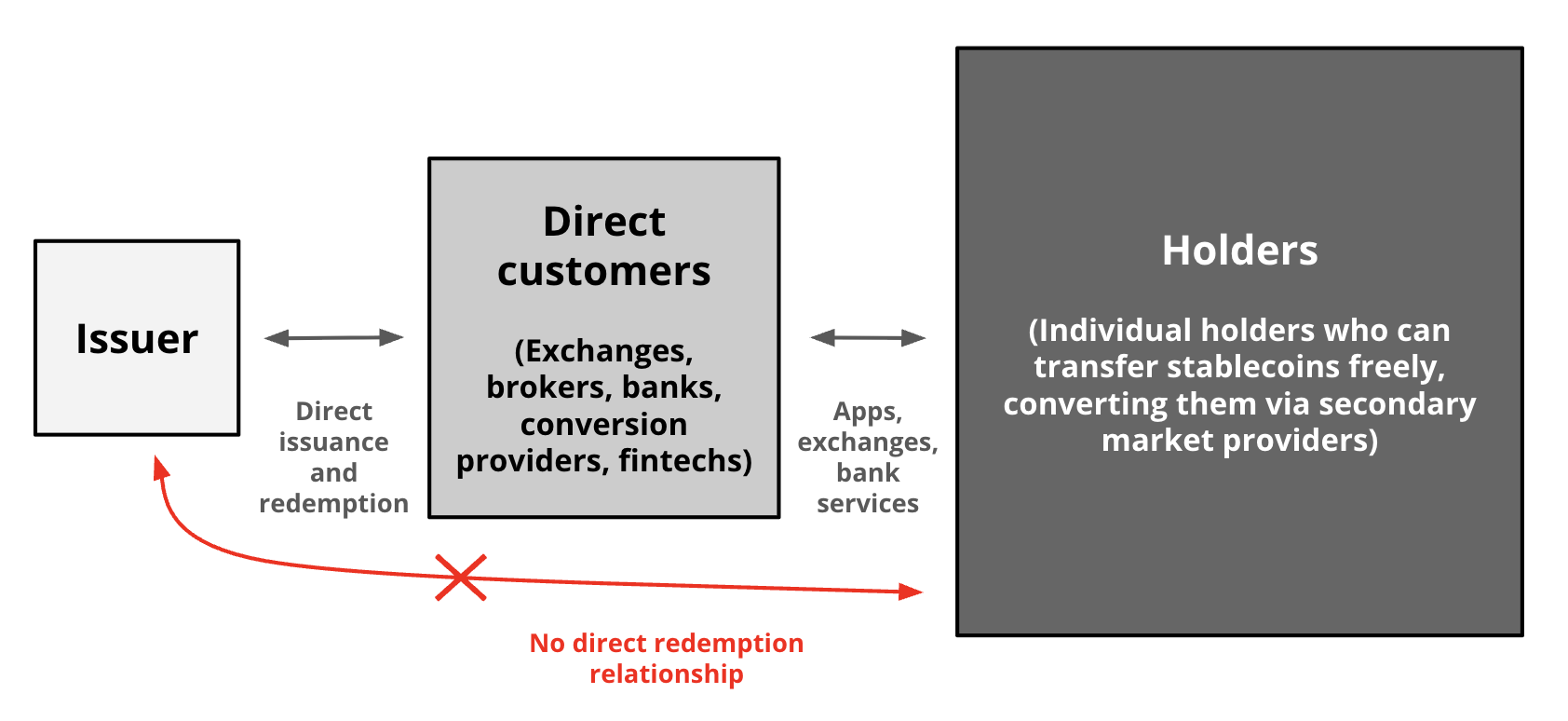

One of the central features of MiCA is its stipulation that holders of stablecoins must be able to redeem directly with the issuer at all times. While this initially seems reasonable, providing the holder with the right to exit, it fundamentally misconstrues how stablecoin issuers and traditional banks operate. Box 2, below, illustrates how stablecoin issuers actually function.

Box 2. The current business model of stablecoin issuers

Entity X is the go-between (for example, an over-the-counter (OTC) brokerage) and comes to an issuer (in this example, Tether), wanting $1 million worth of USDT.

$1 million are sent to Tether’s bank account, and Entity X receives $1 million USDT, and uses it to sell USDT to ‘regular customers’.

That $1 million US dollars is put in Tether’s reserves (with a certain portion held as cash, and a larger portion in US short-term Treasuries and other High Quality Liquid Assets (HQLAs)).

Tether’s revenue equals the yield it generates on top of the principal, while Entity X’s revenue in this case is generated from OTC fees.

If Entity X wants its US dollars back, it can redeem its USDT 1:1 directly with Tether. But this is only because Entity X is not a ‘regular customer’, but rather an institution (for example, Coinbase).

Figure 2. How the stablecoin market functions

As illustrated in Figure 2, a ‘regular customer’ (in other words, retail users) would not be able to mint or redeem directly with Tether. They receive it via intermediaries on the secondary market — Tether is not at all involved in this part. Intermediaries, in this instance, are centralised exchanges (such as Coinbase), decentralised exchanges (such as Uniswap) or OTC desks. Tether, despite its stablecoin being held by 500 million individuals, actually only deals with a small number of these institutional customers, which in turn distribute USDT on the secondary market. However, under MiCA, Tether would need the capacity to comply with KYC requirements, perform AML checks, and onboard every single holder. This operational burden could render the whole stablecoin business model commercially unfeasible.

Universal on-demand redemption also unnecessarily creates a risk that the issuer is forced to sell HQLA below par value. This is particularly likely in a mass-redemption scenario in which failing to meet the regulatory ‘on-demand’ redemption timeframe would be a regulatory breach that would exacerbate market concerns. In the established stablecoin business model, the issuer controls who has access to redemption and when, enabling it to ensure the orderly sale of backing assets and payment to holders. The vast majority of holders must set up their own off-ramps using secondary market providers. The risk is therefore spread throughout the issuer-distributor-holder system. On the other hand, universal on-demand redemption places the risk solely on the issuer. Some commentators have suggested that this secondary market structure would be a better target for regulatory intervention than inventing an impractical and risky universal on-demand redemption right.

Finally, universal on-demand redemption does not actually achieve its objective. In most cases, the holders do not benefit from the right because, before they can use it, they are put through a slow KYC process. By the time KYC is complete, the stablecoin may have depegged, or the reason for wanting ‘on-demand’ redemption may have passed. The requirement, therefore, creates the operational challenges and potential firesale risks above, but with little real upside for holders.

Circle’s EURC, a euro-denominated stablecoin, illustrates this broader misalignment between MiCA’s assumptions and how stablecoins function in practice. While MiCA envisions universal, direct redemption with the issuer at any time, EURC’s redemption process is routed exclusively through Circle France, contingent upon extensive KYC and AML checks and the use of a Single Euro Payments Area (SEPA)-compatible bank accounts. This effectively excludes holders outside the SEPA network, including those in the United Kingdom, the United States, and many other non-European Economic Area jurisdictions, from exercising the right of redemption. This critically undermines the inherent cross-border nature of stablecoins. Consequently, despite being one of the first stablecoins structured to comply with MiCA, EURC represents less than 1% of the total stablecoin market, reflecting insufficient scalability and interoperability of MiCA’s redemption model.

Capital requirements

MiCA also includes capital requirements, which are designed to protect holders from potential losses in the event of issuer default or market stress. Issuers are required to hold 2–2.8% of the average reserve value as capital on their own balance sheets. These rules have their roots in e-money and banking regulation, in which depositor capital is a liability on the balance sheet of the e-money or deposit issuer. While this is not the case here, since issuers are mandated to hold backing assets in custody with credit institutions, which offers ring-fencing of assets from the issuer’s operating assets to some extent, we would argue that more protective capital requirements make logical sense. However, tying capital requirements to issuance does not, as will be explained later.

The reason that more protective capital requirements make sense here (than compared to the UK’s case) is that MiCA is an EU regulation, not a property law statute. Whether segregated assets held in custody are genuinely insolvency-remote depends on how the national law of the relevant member state treats custodial arrangements. In the event of an issuer’s insolvency, a state court may rule that backing assets do not belong to holders.

Although strict regulation is not inherently bad for an emerging technology, it is clear that this regulation has stifled the growth of euro-denominated stablecoins. Overbearing regulation like MiCA risks regulatory arbitrage where entrepreneurs relocate to more favourable jurisdictions.

The United States’ GENIUS Act

While the EU’s regulatory model covers ‘digital assets’ more broadly, the United States’ Guiding and Establishing National Innovation for U.S. Stablecoins Act (more commonly known as the GENIUS Act) establishes the first comprehensive federal regulatory framework specifically for stablecoins. It is much less prescriptive than MiCA, instead regulating from a principles-first approach.

The GENIUS Act introduces a range of requirements for stablecoin issuers, focusing primarily on transparency, consumer protection and financial stability. It mandates that stablecoin issuers hold 100% of their reserves in cash, US Treasuries, or other similar low-risk assets, so that issuers can meet redemption requests at any time. To enhance transparency, the Act requires issuers to publish monthly attestations on their reserve assets, audited by a registered public accounting firm. Moreover, issuers are required to have the technological capacity to freeze and seize stablecoins in compliance with lawful orders to combat illicit activities. Stablecoin holders are also prioritised in the event of an issuer’s insolvency, ahead of any other creditors. Unlike MiCA, the GENIUS Act neither mandates universal on-demand redemption, preserving the business model of issuers, nor does it include capital requirements.

This principles-based model has been praised for providing much-needed clarity, while also being flexible enough to allow the market to evolve. By focusing on the quality of reserves and federal oversight, the GENIUS Act successfully enhances the legitimacy of stablecoins and mitigates some of the most immediate systemic risks.

However, the GENIUS Act is not without its flaws. Critics have cited its provision allowing uninsured deposits in commercial banks to be counted as permissible reserve assets as being potentially harmful to financial stability. In a scenario of banking stress, stablecoins backed by such deposits could face a confidence crisis and become prone to runs, potentially undermining the very stability the Act seeks to ensure.

It is also worth noting that the US regulatory picture on stablecoins extends beyond the GENIUS Act. The Digital Asset Market Clarity Act, which passed the House of Representatives in July 2025, is currently stalled in the Senate over whether third parties — such as exchanges — should be permitted to offer yield on stablecoin holdings. While the GENIUS Act prohibits issuers from paying interest, a perceived loophole allows third-party platforms to offer rewards on stablecoin balances — and the Office of the Comptroller of the Currency has since issued proposed rulemaking that would presume certain such arrangements to be in violation of the Act’s ban. White House-brokered negotiations between the banking and crypto industries have so far failed to produce a compromise. This fast-moving dispute highlights the difficulty of drawing clean lines between stablecoins as payment instruments and stablecoins as savings-like products.

MiCA and the GENIUS Act illustrate two differing approaches to stablecoin regulation. It is now up to the UK to draw lessons from each to produce a regime that promotes innovation, upholds consumer welfare, and ensures financial stability. The UK has just closed its consultation stage, with regulators now reviewing advice from firms and policy advisors in order. In the following section, we shall examine what has been proposed so far, while also evaluating the likely effectiveness of such proposals.

What proposals have been made in the UK for regulating stablecoins?

The UK’s regulatory response is being shaped jointly by the Financial Conduct Authority (FCA) and the Bank of England (BoE). The FCA is responsible for ensuring the smooth functioning of financial markets and the protection of consumers; while the BoE is concerned with the overall stability of the UK’s financial system.

Financial Conduct Authority proposals

In May 2025, the FCA released a consultation paper on stablecoin regulation. The proposals it makes are a positive start in laying the groundwork for a successful regulatory regime. The FCA identifies some core principles needed to build trust in any new form of digital money — a non-negotiable right to redemption at par, the legal certainty of holding backing assets in HQLA in a statutory trust, and the importance of independent custody to prevent the misuse of funds.

Founders of some of the UK’s most significant FCA-approved stablecoin startups have broadly welcomed the proposals. As Andrew Mackenzie, Founder and CEO of Agant Finance, told us: “The developments from the FCA and BoE are overwhelmingly positive. They have real concerns over the effects of stablecoin growth on credit creation in the UK, but equally are listening to the advice of industry leaders on the potential for stablecoins to deliver meaningful innovation and benefits to the UK economy. With a few tweaks to both regimes, Agant is highly optimistic about the part that GBP stablecoins will play in the UK’s future.”

Meanwhile, Benoit Marzouk, Founder and CEO of Tokenised GBP, said: “Although there has been some criticism of the FCA, it is the regulator’s job to mitigate financial risk. We are confident that the FCA will get it right.”

Despite this, our research and industry input identified several key issues that may leave the UK significantly disadvantaged compared to the US. For instance, the FCA proposes universal on-demand redemption rights for all holders of a stablecoin, which, as explained in the MiCA section above, is not only operationally burdensome and expensive for issuers, but also fundamentally departs from how issuers operate and risks hampering innovation by favouring larger, more established issuers.

Overly stringent redemption times

Another proposal the FCA makes that would limit the UK’s stablecoin industry concerns its T+1 redemption rules, which mandate redemption one day after a request has been made. Money Market Funds (MMFs) and even highly liquid gilts cannot necessarily be liquidated T+1, especially under stress events. This may force issuers to hold too much cash relative to yield-bearing — and therefore revenue-generating — assets, such as gilts. If the FCA allowed more lengthy redemption times and permitted issuers to reserve T+1 or T+0 redemption for those customers who pay a premium fee, it would be much more commercially viable for issuers. It would also allow issuers to better allocate resources to large or urgent redemption requests, which supports secondary market price stability. There is an emerging consensus among industry participants that regulators would benefit from creating more flexible principles, such as those in the GENIUS Act, rather than prescribing ideal business models before viable market practices have been given time to develop.

Issuance-linked capital requirements

The FCA’s proposals also outline bank-like capital requirements for issuers, which in and of themselves are a fair requirement. However, certain capital and own funds requirements — specifically the K-SII K-factor requirement — tie capital to the amount of stablecoin issued. A British stablecoin issuer would be required to raise ‘own funds’ (generally meaning ordinary shares or retained profits) of the largest of:

£350,000 Permanent Minimum Requirement (PMR);

Three months of the firm’s fixed expenditures (Fixed Overhead Requirement); or

Two percent of the average value of stablecoins the firm has issued (K-Factor Requirement).

This requirement stems from e-money and banking regulation, where capital acts as a loss-absorbing buffer. An own funds requirement can significantly reduce risk where the company’s assets could fall in value (such as bank mortgages), and the balance sheet is funded primarily by short-term liabilities (such as e-money or demand deposits). By requiring the balance sheet to be funded with a portion of equity or retained profit, a loss in the value of assets is borne as a loss in equity value rather than pushing the company into insolvency as would be the case for balance sheets funded 100% by on-demand liabilities.

However, in the context of British stablecoin issuers, this ignores the legal robustness of the proposed backing asset model. Under the FCA’s own guidelines, backing assets must be held in a statutory trust. This creates a proprietary claim for the token holder; the assets effectively do not belong to the issuer, do not sit on its balance sheet, and are legally ring-fenced from the issuer’s creditors in the event of insolvency. This provides a superior level of property right protection compared to the contractual segregation models found in many civil law jurisdictions (such as under MiCA in the EU). Because the assets are legally safe from risks to the issuer’s own assets, requiring the issuer to hold a separate, multi-million-pound equity buffer proportional to issuance is a category error.

Furthermore, the proposal relies on a fallacy. It assumes that holding regulatory capital guarantees that liquid cash is available to pay redemptions or pay for an insolvency process. In reality, capital requirements dictate how a business is funded (equity versus debt), not what assets it holds. A firm could meet the 2% requirement by raising equity funding, but then spend that cash on illiquid assets (like computers) or consumables (like salaries and legal fees). Therefore, the K-SII K-Factor Requirement creates a high barrier to entry without necessarily providing any additional support to cover redemptions or pay an administrator to return funds to users.

Instead, the primary risk capital requirements mitigate is operational — specifically, the cost of winding down the firm if it fails. By structuring the funding to include a portion of equity rather than debt, the requirement ensures there should be some assets left to liquidate (and pay wind down costs) once all creditors have been paid off. Crucially, this cost does not scale linearly with the amount of stablecoins issued. Because stablecoins operate on automated digital ledgers, winding down a fund of £1 billion does not cost 10 times as much as winding down a fund of £100 million. Consequently, a flat 2% tax on issuance is illogical. The Fixed Overhead Requirement, which mandates holding three months of operating costs as liquid cash, is already the appropriate tool to cover wind-down costs, rendering the issuance-linked K-Factor Requirements redundant.

Finally, this requirement introduces two significant negative side effects:

Systemic risks. By capping issuance based on the issuer’s capital, the regulator creates an artificial supply cap. If market demand for the stablecoin rises but the issuer cannot mint more tokens because they haven’t yet raised the requisite capital, the secondary market price will rise above the £1 peg. This forces users to overpay and breaks the fundamental promise of stability.

Anti-competitive effects. The requirement for specific high-quality capital (Common Equity Tier 1) heavily favours incumbents with large, existing balance sheets. While established firms can meet this rule using retained profits, startups cannot easily raise this specific form of capital from investors. This creates a punitive barrier to entry, entrenching market leaders and stifling innovation.

To be clear, we are not arguing against capital requirements as a protective measure. Rather, tying capital requirements to issuance specifically is the issue at hand, which both fails to deliver what it intends to achieve and also actively increases risk for issuers and consumers.

Interest

Finally, the FCA, being the conduct-focused regulator, also bans issuers from passing through interest earned on reserve assets, suggesting stablecoins should function as transactional instruments akin to traditional e-money, rather than savings or investment products like bank savings accounts. While this aligns with international concerns over financial stability, this blanket prohibition risks distorting competition and pushing users towards riskier, less transparent offshore products. It also codifies a questionable competitive advantage for bank deposits at a time when they could face healthy, competitive pressure from stablecoins. As such, a more flexible approach should be explored, permitting interest-bearing features with enhanced governance for specific use cases like institutional treasury management. This would support responsible product development and market competition, and prevent regulatory arbitrage without compromising the regime’s core stability objectives.

Bank of England proposals

The FCA’s proposals, as outlined above, cover ‘non-systemic’ stablecoins. Those that become systemically important are regulated under the BoE regime, provided that they are deemed systemic by HM Treasury. Complementing the FCA’s May consultation paper, the BoE released its own on 10 November 2025, focusing exclusively on sterling-denominated stablecoins designated as systemic.

Deposits held at the Bank of England

The BoE regime would require issuers to hold a minimum of 40% of the backing assets in unremunerated deposits at the BoE, allowing up to 60% in short-term gilts. Although forcing the issuer to hold unremunerated reserves removes 40% of the issuer’s potential revenue, allowing issuers’ accounts at the central bank level is a significant, and indeed globally leading, step — no other regime has allowed this. Central bank reserves almost eliminate the credit and liquidity risk associated with backing assets. However, the consultation paper provides no reasoning for how it formulated the 60:40 split. As such, projections assessing issuer commercial viability would appear necessary to justify such an approach.

Caps

The proposed regime would also implement caps on the maximum amount to be held by individuals (£20,000) and corporates (£10 million). On the one hand, this is a move to mitigate the risk of rapid and destabilising deposit outflows from commercial banks into stablecoins. However, it also undermines commercial viability. Given that some of the most promising and truly innovative use cases for stablecoins are in corporate treasury and B2B payments, which regularly involve transactions and holdings that are orders of magnitude larger than the proposed £10 million cap, these caps risk severely constraining stablecoin adoption and development. The paper notes that some exemptions may apply, for example, for retail-facing corporations (such as a supermarket), but it is unclear to whom else these may apply.

The caps also pose a significant risk to the functioning of the secondary market. Holders and distributors of stablecoins would not be able to buy and sell in the amounts needed to meet market demand. The stablecoin’s price on exchanges would potentially oscillate as the market jumped from shortage to surplus rather than responding smoothly, which would involve exceeding the proposed limits from time to time.

Moreover, the BoE’s move to impose these caps arguably undermines its mandate to regulate ‘payment systems’. By imposing caps for holders, they blur the lines between their own mandate and that of the FCA, which exists to regulate conduct and protect consumers, including setting rules that affect end-users. Proponents would argue that this is not a conduct rule, but a macroprudential tool necessary for its core mandate of protecting the UK’s financial stability. However, it can be seen that the caps are far too conservative, potentially wiping out entire commercial business verticals. It is also unclear how the BoE plans to impose these caps — do they have the technological capacity to analyse the blockchain, and which entities would need to enforce the limits, given that the wallet providers are separate from the issuers?

Systemic designation

There is also a question over when and how a stablecoin is deemed ‘systemic’. The consultation paper notes that the decision lies with HM Treasury, but it views the ambiguity as a feature, not a bug, giving regulators leeway to make judgements and recommendations. For innovators, though, clear rules and predictable thresholds are paramount. If the trigger for being subjected to the more stringent BoE regime is a discretionary judgment call, it creates a significant regulatory uncertainty for any stablecoin project. On the other hand, if payment processors are anything to go by, American Express is still not deemed as a systemically important Financial Market Infrastructure by the Payment Services Regulator, despite having a large presence in the UK, perhaps highlighting the extent of market penetration required to be deemed as such.

How should the UK regulate stablecoins?

Given the different regulatory approaches taken by jurisdictions around the world, our stance on how the UK should proceed is as follows: we believe that MiCA is too prescriptive and the rules are too restrictive, and that the GENIUS Act, while superior, is currently too laissez-faire. Thus far, the UK is moving in the right direction, but proposals put forward by the FCA and BoE have considerable drawbacks.

The Chancellor recently announced that bringing cryptoassets into the “regulatory perimeter” is “a crucial step,” and, similarly, the FCA has made stablecoin regulation an explicit priority for 2026. It is also encouraging to see world-leading ideas being introduced, such as having issuers keep a portion of their reserves directly at the BoE, which highlights the extent to which stablecoins are being taken seriously.

However, the current proposals also have their flaws, and, if implemented in their current form, would make it difficult for entrepreneurs to thrive. Careful tweaks are therefore required by regulators to ensure the best possible regulatory regime. Time is also of the essence, with other countries forging ahead of the UK. A genuinely pro-innovation regime must embrace the core stablecoin business model, ensure commercial viability, and provide entrepreneurs with clear, enabling guardrails.

Below, we set out seven key recommendations that would enable the UK to preserve its longstanding leadership in global finance, strengthen sterling’s digital relevance, and attract the next generation of financial innovators.

Adopt a principles-based approach to regulating stablecoins. Firms in emerging sectors need flexibility to adapt technology and business models. As such, regulators should adopt higher-level, principles-based rules that support innovation while still securing core regulatory outcomes. This can likely be achieved through alignment in approaches between the Financial Conduct Authority (FCA) and the Bank of England (BoE).

Scrap universal redemption. Universal on-demand redemption misunderstands how stablecoin issuers operate and should be replaced with a model reflecting the current structure of issuers, distribution partners, and users.

Remove bank-like capital rules. Capital requirements designed for banks are inappropriate for fully backed issuers, and should be replaced with oversight focused on reserve quality and transparency.

Allow flexible redemptions. Flexible redemption timelines should be introduced, as seen in the GENIUS Act, to support issuer sustainability and market resilience.

Lift holding caps. The £20,000 (individual) and £10 million (corporate) limits should be lifted, as they are currently overly restrictive and risk stifling institutional and business-to-business innovation, as well as creating secondary market price volatility and liquidity shocks.

Explain reserve split. The reasoning behind the 60:40 reserve rule should be clarified, and regulators should consider remunerating a portion of the 40% held at the BoE to maintain commercial viability.

Exempt small businesses. As happens with payment services and other regulatory regimes, small businesses operating within the stablecoin market should be exempt from more stringent regulatory expectations to allow them to balance costs and innovation, which is particularly important in a nascent and fast-developing industry.

Conclusion

As stablecoins redefine global finance, the choices made now will determine whether the UK leads or lags. While the FCA and BoE’s intentions to ensure stability and consumer protection are laudable, their proposals in their current form fall short. The UK must avoid repeating the EU’s over-prescriptive MiCA model and instead adopt a pragmatic, principles-based approach similar to the United States’ GENIUS Act.

A genuinely pro-innovation regime should embrace the stablecoin business model, ensure commercial viability, and provide entrepreneurs who are currently building in the dark with clear, facilitative guardrails. These guardrails should enable rather than inhibit growth. If designed correctly, such a framework could allow the UK to continue its long-standing leadership in global finance, strengthen sterling’s digital relevance, and attract the next generation of financial innovators.

acknowledgements

The report was authored by Hugo Okada and Osian Guthrie, undergraduate students at the University of St Andrews and Co-Presidents of its Blockchain Society, who have previously worked for Blockchain.com and Agant Finance, respectively. It was edited by Eamonn Ives, Research Director at The Entrepreneurs Network.

The authors would like to acknowledge the following individuals for their insights and contributions, which proved invaluable during the research for this paper:

Adam Jackson — Chief Strategy Officer, Innovate Finance, and Head of Digital Pound Foundation

Laura Clatworthy — Head of Digital Assets and Emerging Tech, Edwin Coe LLP

Adriana Ennab — Director, Stand With Crypto UK

Simon Jennings — Executive Director, UK Cryptoasset Business Council

Tom Rhodes — Chief Legal Officer, Agant Finance

Joey Garcia — Executive Director, Chief Strategy, Policy, Regulatory Affairs Officer, Xapo Bank

Lord Holmes of Richmond OBE — Member of the All-Party Parliamentary Group on FinTech and the All-Party Parliamentary Group on Digital Identities

Andrew MacKenzie — Founder and CEO, Agant Finance

Benoit Marzouk — Founder and CEO, Tokenised GBP

Dr Lisa Cameron — Former Chair, Crypto and Digital Assets APPG

Kaitlin Argeaux — Founder and CEO, CryptoMondays London

Nic Carter — Partner, Castle Island Ventures

Helen Disney — Founder and CEO, Unblocked

Any errors of fact or judgment are the authors’ alone.